Throughout the ages, those in power have sought to raise revenue by various means. Broadly speaking, following the Civil War and Restoration, Parliament would determine the personal income of the monarch. If the ruler then wished to raise more money for something exceptional, such as a war for example, he would have to apply to Parliament for it. This was an attempt to rein in the power of the king, as monies were only provided for specific reasons, and had to be spent appropriately.

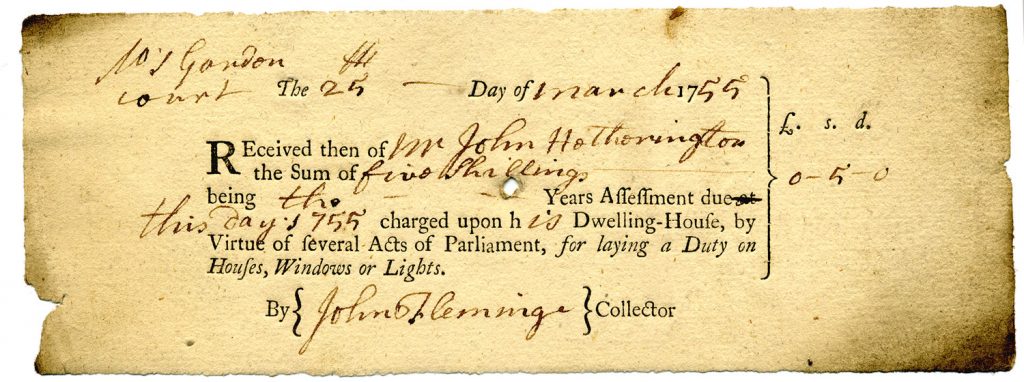

Nowadays everyone expects to pay income tax on their earnings, but in the past no one would have countenanced such a thing. It would have been considered too intrusive, and indeed would have been ridiculously expensive and almost impossible to enforce. Instead monies were raised in a number of ways, including borrowing, customs duties (as unpopular now as always), land taxes from 1667 in Scotland and 1692 in the rest of Britain, and hearth taxes at 2s per annum for each hearth in a house from 1662 (except in Scotland).In The Ladies’ Tale I mention the Window Tax. This was a real tax, which was introduced by King William III in England, Wales and Ireland in 1696, and in Scotland from 1748. This was intended to cover the cost of reminting damaged and clipped coinage. Whilst it might now seem bizarre, it was intended originally to be a relatively fair tax as it was thought it would not impact on the poor too much. Every inhabited dwelling was charged two shillings a year. Cottages, which were houses where the inhabitants were too poor to pay church or poor rates, were exempt.

In addition to this, larger houses were additionally taxed based on the number of windows in the property. Houses with less than ten windows did not pay window tax. Those with 10-20 windows paid four shillings, and those with 20-30 windows paid eight shillings. In addition to the apparent fairness, the tax was easy to calculate, as it could be assessed from the outside without having to involve the taxpayer directly, and it seemed impossible to avoid paying. As there was no strict definition of a window in the legislation, the smallest opening (even a perforated grate in the wall) was often classed as a window and taxed. Roman Catholics and aliens were even harder hit, as until 1830 they had to pay double tax!

Needless to say, people were not happy at this new tax, and soon started trying to find ways of avoiding it nonetheless. The obvious way was to brick up some of the windows, and evidence of this can still be seen in a good number of Georgian houses. In Scotland many windows were painted black rather than being bricked up. Others would have one huge window frame containing several glassed areas separated by brick, hoping it would be classed as one window. The government got round this one by stating that bricked separations of 12 inches or more meant each glassed area counted as a separate window.

As early as 1718 revenue was declining noticeably due to the blocking of windows, and new houses were being built with fewer windows to avoid the tax. Whilst it did not necessarily impact the rural poor too much, for the urban poor this was a different matter. In towns people were more likely to rent a room or rooms in a larger building or tenement. However, the number of windows were not assessed according to households, but by the whole building, the landlord paying. This often resulted in one of two things: either the landlord would raise rents to cover the cost of the tax, or would brick up many of the windows in the building, which meant that many families were left with no light or ventilation in their homes.

This caused a great many protests, as the window tax became thought of as a tax on air and light, and undoubtedly led to a rise in sickness and death. In a sanitary report about Sunderland in 1845, it was stated that: ‘that the blocking up of the numerous windows caused by the anxiety of their owners to escape the payment of the tax, has, in very many instances, greatly aggravated, and has even…in some cases been the primary cause of much sickness and mortality.’

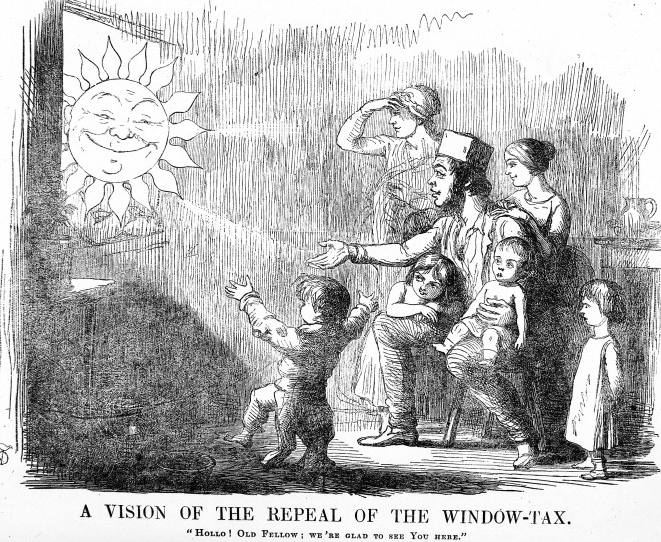

The tax was raised a number of times during its existence, six times between 1747 and 1808. The industrial revolution, which resulted in mass migration from countryside to town in the nineteenth century, exacerbated the problem of overcrowding, and led to increasing pressure from medical people and more enlightened souls for a repeal of the window tax, which was making the problem even worse, as it encouraged damp and foul air.

The tax was halved in 1823, but following continued and relentless campaigning, was finally abolished in 1851, and was replaced with a house tax.

For my part, although I’ve never lived in a house with no windows, when I travelled in India I did stay in interior hotel rooms, which had no windows at all, and it was an unpleasant, claustrophobic experience. I would wake up and would have no idea what time of day it was, and spent as little time as possible in my room. It would be horrendous to live in a home that was permanently pitch black!

{kind=link}

4 Comments

Extremely interesting! Thank you as always for the wonderful blog!

Thank you! SO glad you enjoyed it!

I’ve always been curious about this. Thanks for such a thorough explanation!

You’re most welcome. I’m glad you found it helpful!